Archive for the ‘compensation’ Category

Loblaw Compensating Bangladesh Victims

Filed under: brands, charity, compensation, consumers, corporate citizenship, disaster, employees, international, retail, workplace safety |

Comments (4)

Comments (4) Canadian grocery chain Loblaw has announced that it will compensate the families of victims of the factory collapse that happened in Bangladesh’s Rana Plaza this past May. The factory housed a number of garment factories, including some that made garments for the Canadian’ retailer’s “Joe Fresh” line of clothing.

Some will worry that this is a case of too little, too late. And certainly the “too late” part is correct. Compensation is always a distant second best when compared to avoiding deaths in the first place. Whether the compensation is “too little” or not is subject to debate. It’s not clear that Loblaw (or any company) bears direct responsibility for the behaviour of the companies it buys services from, though certainly the case is stronger where the buyer is a highly-capable multi-billion dollar company, and when the companies it buys from are smaller, less-capable companies operating in an under-regulated environment.

Either way, it’s hard not to admire the company for stepping up and assuming responsibility. And the money will surely be a godsend to the families of the victims. But the real benefit of the compensation scheme may well lie in its capacity to reassure Canadians (and other westerners) that the company cares, and that things are going to get better in Bangladesh, so that we can all keep buying goods made there. Because that’s what Bangladesh truly needs.

But on the other hand I continue to worry about Bangladeshi exceptionalism — that is, that all the attention being lavished on the garment industry in Bangladesh will mean little attention gets paid to parallel problems in places like Malaysia, Vietnam, Pakistan, China, and a number of African countries. There are surely factories in many, many developing countries that are ‘Rana Plazas’ just waiting to happen. It’s not clear just what is being done about those.

Finally, many will be asking what still needs to change? Two things come to mind. The first is that companies like Loblaw need to keep getting better at vetting the companies they do business with, in order to weed out the bad ones. This, of course, is much harder than it sounds. The second is that Canadians and other Westerner consumers need to change the way they think about the issue. They need to recognize that Bangladesh is not Canada, and doesn’t have the luxury of North American-style labour standards. They will surely get there, but it will be a long, slow climb.

Most important is that this tragic series of events has focused the world’s attention on an important set of issues. But the challenge lies in harnessing that attention and seeking out reasoned discussion, rather than knee-jerk reactions.

CEO Pay for Performance in Canada

CEO pay — in Canada, at least — is apparently more closely aligned with corporate performance than most people have suspected.

Last week I had the pleasure of hosting Matt Fullbrook, Manager of the Clarkson Centre for Business Ethics and Board Effectiveness, as part of my Business Ethics Speakers Series. Fullbrook’s presentation focused on an interesting study recently completed by the Clarkson Centre.

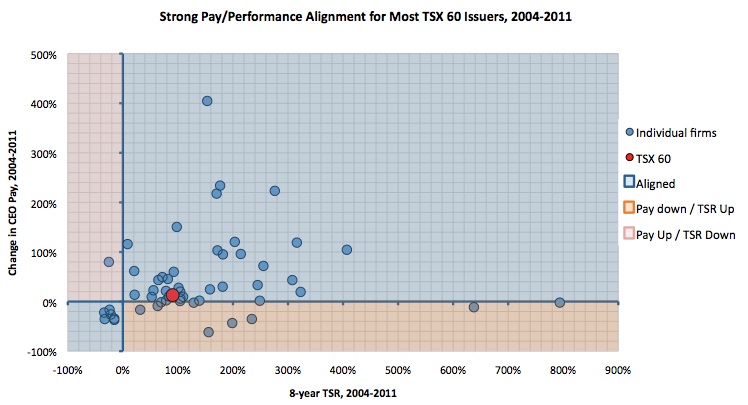

Much of the discussion focused on this provocative graph:

The graph plots change in CEO pay against total shareholder return (TRS). Each dot represents a company listed on the TSX 60. The red dot shows the average for all companies studied. The blue shaded areas indicate companies at which CEO pay and shareholder value have been headed in the same direction (up or down) over the 8 years under study (2004-2011). The other areas show misalignment. The vast majority of companies are in the blue regions. Only at one company did pay rise substantially without a commensurate rise in shareholder value, and several companies showed phenomenal growth in value with no change in CEO compensation.

After his presentation, Fullbrook summarized the study’s findings for me this way: “Our research shows that CEO pay and performance are largely in sync at Canada’s largest corporations, contrary to conventional wisdom. Despite the Financial Crisis, and a significant amount of CEO turnover, most issuers have successfully aligned executive compensation with shareholder returns, which is great news for investors.”

I’ll leave you with just a couple of comments on this.

First, it’s worth noting that the x-axis on the graph above shows change in CEO pay, rather than absolute level of CEO pay. So while we can see that not many Canadian companies provided their CEOs with big raises, that doesn’t mean that they weren’t overpaid to start with. They may or may not have been; that’s a different study. But the fact that pay and performance are heading in the same direction is still pretty significant, given that lots of criticism has been rooted in the perception that CEO pay was climbing while investors get shafted. This study shows that, in general, that’s not true in Canada.

Second, just what counts as “alignment” is itself a difficult question, and during his presentation Fullbrook was thoughtful in this regard. What we see in the red dot in the graph above is a kind of correlation. It suggests that the pattern in Canada is that a slight upward trend in CEO pay is accompanied by a bigger upward trend in shareholder value. But this leaves open questions such as whether TRS is the right measure of “performance” (even if we focus exclusively on the interests of shareholders).

And if we try looking at individual companies, at a particular moment in time, the question of alignment becomes even more difficult. The word “alignment” itself arguably suggests parallel trajectories. But where a CEO is overpaid, it makes sense for pay to go down even while (hopefully) value is going up. The attempt there is to make pay commensurate with value, not to push them in the same direction.

Executive compensation continues to be one of the hardest problems faced by corporate boards, as well as an absolutely key ethical obligation. Doing it well is difficult when we’re not even sure what doing it well looks like.

NHL Lockout and the Ethics of Labour Disputes

Filed under: accountability, adversarial ethics, capitalism, compensation, justice, sports, stakeholders, unions, wages |

Comments (4) When the rich and powerful butt heads, are they obligated to look out for the little guy?

The NHL lockout may be over, but its impact is far from forgotten. Or even clear. And the impact goes far beyond the loss of income to the NHL, its member teams and its players.

The end of the dispute may mean little to the economy as a whole, but to one portion of the economy — the portion that depends for its livelihood on the actual playing of hockey games — it means everything. The economic loss to Canada as a whole as a result of the loss of half a season of hockey may amount to less than 0.05 per cent of GDP, but the impact was felt disproportionately by the thousands of businesses and individuals that depend for their livelihood on the NHL and its players. For every Sidney Crosby or Daniel Alfredsson making millions on the ice, there is an entire ecosystem of managers, announcers, hotdog vendors, and Zamboni drivers who only have jobs because hockey is being played.

The lockout resulted, in other words, in a lot of so-called ‘collateral damage.’ Some teams had to lay off staff (in some cases, that meant hundreds of employees per team) and many businesses — from sports bars to the guy selling hotdogs outside the arena — saw business dip or even bottom out entirely.

Of course, this is true in almost any labour dispute. When auto assembly-line workers go on strike, workers at companies that manufacture parts for those assembly lines may see hard times as a result. But as many have pointed out, the dispute between the NHLPA and the NHL was a dispute between millionaires and billionaires, which gives the whole thing a distinctly different feel.

Whether the 113-day dispute was worthwhile to either the players or the league — whether either side gained more than it lost — is for them to decide. The relevant ethics question, here, is what part the financial fate of these innocent bystanders should have played in the decision making of the two parties to this dispute, namely the NHL and the National Hockey League Players’ Association (NHLPA). Should the league and players have felt any obligation to end the dispute early, in order to limit financial collateral damage?

It is tempting to cast this question as a matter of what economists call ‘externalities.’ Externalities are the effects that an economic transaction has on non-consenting bystanders. Pollution and noise are standard examples. And both economic theory and ethical theory agree that externalities are a bad thing. It is typically both inefficient and unfair if significant costs are foisted on innocent bystanders.

But economic theory, at least, doesn’t typically count the income effects of competitive behaviour as “real” externalities. If I outbid you in an auction, your interests have been harmed but not in a way that results in either economic inefficiency or real injustice. If I invent a better mousetrap and put makers of lesser products out of business, the result is ‘frictional’ unemployment but also long-term social gain. And during a labour dispute, money not being spent on hockey-arena hotdogs or Zamboni-driver wages are surely being spent on something else: one man’s loss is another’s gain.

But while not technically unfair, the outcome for bystanders is certainly unfortunate, a bad thing by almost any measure even if not the result of wrongful behaviour. And when the dispute at hand is between millionaires and billionaires, it’s worth asking at least whether the rich don’t have some duty, some social obligation, to take better care of those less fortunate.

Once upon a time, the rich and powerful cleaved to the notion of ‘noblesse oblige,’ the idea that with wealth and power come responsibility. Of course, even if the team owners and the players took such social obligations seriously, that doesn’t necessarily mean the dispute would have ended earlier. An obligation to look out for the little guy doesn’t mean an obligation to throw in the towel. But the notion of social responsibility, not to say humility, might well have done something to reduce the length, and impact, of what many regard to have been a pointless conflict in the first place.

Executive Compensation at a Regulated Monopoly

Filed under: accountability, activism, boards, CEOs, compensation, consultants, governance, shareholders, stakeholders |

Leave a comment Protests broke out last week at the first annual shareholders’ meeting of Canadian energy company, Emera. Emera is a private company, traded on the Toronto Stock Exchange. But one of its wholly-owned subsidiaries, Nova Scotia Power, is the regulated company that supplies Nova Scotia with virtually all of its electricity.

The protest concerned the fact that several Emera and Nova Scotia Power executives had received substantial raises, despite the fact that Nova Scotia Power had just recently had to go to the province’s Utility and Review Board to get approval to raise the price it charges Nova Scotians for electricity. According to the utility, the rate hike was needed to add new renewable energy capacity to Nova Scotia’s grid. But protestors wondered if the extra cash wasn’t going straight into the pockets of wealthy executives.

The first thing worth pointing out for anyone not already aware is that practically no one thinks that anyone is doing executive compensation particularly well. Sure, most boards have Compensation Committees now, and many big companies engage compensation consultants to do the relevant benchmarking and to make recommendations. But no one is particularly confident in either the process or the results. So Emera’s board is far from alone in facing this kind of critique.

The second point worth making is that there are two very different kinds of stakeholders concerned in a case like this, but in this particular case they happen to overlap substantially. On one hand, there are Emera’s shareholders. They have an interest in making sure the company’s Comp Committee does its job, and sets executive compensation in a way that attracts, retains, and motivates top talent in order to produce good results. On the other hand, there are customers of Nova Scotia Power, ratepayers who want a cheap, stable supply of electricity. Now, as it happens, many of the vocal protestors at Emera’s annual meeting are members of both groups: they are shareholders in Emera and customers of Nova Scotia Power. But it is crucial to see that these are two separate groups, with very different sets of concerns. When this story is portrayed as a story about angry shareholders, this crucial distinction gets blurred. What’s good for shareholders per se is obviously not the same as what is good for paying customers. And, importantly, a company’s board of directors aren’t accountable to customers in the same way that they are to shareholders.

The final point to make about this is that, to observers of corporate governance, this is actually a “good news” story. As noted above, no one thinks executive compensation is handled very well. But despite that fact, corporate boards still face relatively little pushback from shareholders, and are relatively seldom held to account in this regard. There are of course exceptions (including a number of failed “say on pay” votes) but those exceptions prove the rule. And that’s unfortunate. In any ostensibly democratic system, it is a good thing when the voters take the time to show up and to ask hard questions. Even if no one is sure that such participation improves outcomes, it is an invaluable part of the process.

———-

(I was on CBC Radio’s Maritime Noon show to talk about this controversy. The interview is here.)

———-

Healthcare, Unions, and Selling Donuts to Canadians

Filed under: compensation, employees, health, pay, unions, virtue, wages |

Leave a comment Selling donuts to Canadians sounds so easy that it seems like the punch-line to a not-very-funny joke.

Apparently, however, it isn’t always such and easy thing to do. Or at least, not easy enough to support paying double the minimum wage to the people who serve the donuts. Witness the case of the three Tim Hortons kiosks at Windsor Regional Hospital (in Windsor, Ontario, just across the border from Detroit, MI). At Windsor Regional, the donut-and-coffee kiosks are a big drain (to the tune of a quarter-million dollars a year) rather than a source of revenue. Part of the reason, apparently, is that the servers who work there are paid over $20/hour — far above Ontario’s minimum wage of $10.25. The kiosks are in effect being driven under by their own employees.

Part of the complexity of this story lies in the fact that the donut kiosks in question are at a hospital. So this isn’t just a question of a profit-hungry capitalist at odds with unionized employees. The cost overrun in this case is borne by the hospital, a not-for-profit organization that must recoup the cost in other ways.

The donut kiosks, along with other food service outlets at the hospital, are part of the organization’s overall operating budget, part of the overall cost of providing healthcare to the people in the hospital’s catchment area. As Canadian health economist Robert Evans has often pointed out, every dollar spent on healthcare is a dollar of income for someone. The result is that there are plenty of people — some wealthy, and some not so wealthy — with a vested interest in not reducing the cost of healthcare. That’s not a matter of malice; it’s just a matter of math.

But of course, the salaries of unionized employees can only be part of the tale, here. If the three kiosks have, say, two employees on duty at a time, then paying each of them only minimum wage would still only save about $120,000 — which accounts for less than half of the shortfall. So it doesn’t make sense to point to the workers’ wages as “the” cause of the problem. The supply of donuts and coffee at Windsor Regional simply seems to be out of line with demand.

Of course, one way out would be for the coffee kiosks to raise their prices. That may or may not be permitted by Tim Hortons’ franchise agreement. But anyway, raising prices would mean pushing the burden onto patients and their families along with hospital staff. And at most hospitals, the on-site food outlets have a virtual monopoly, which puts customers at a serious disadvantage. It also means that demand at a hospital is less elastic, which means the hospital kiosks have more power to raise prices than a non-hospital donut seller would. And if you believe that the wage currently being paid is a fair one (by some measure), then that’s what should be done. They should raise prices to benefit employees at the expense of patients, families, and staff.

All if this just illustrates that idealism about fair wages has its limits. In a world of limited resources — i.e., the world we live in — giving more to one person often means taking more from someone else. The result is that you can’t argue for higher (or lower) wages without talking about prices. Wages are part of an economic system, and discussions of justice in one part of that system can’t ignore justice in the others.

———-

(Thanks to Prof. Alexei Marcoux for pointing out this story to me.)

Did Apple’s CEO Forego $75 million as a Matter of Principle?

There’s tone at the top, and then there’s tone at the top of the top. And when it comes to defining “top,” it’s hard to beat being the highest-paid CEO in the world, leading the most valuable company in the world. The man who occupies that post, of course, is Apple Inc.’s Tim Cook.

And recently, Cook made a pretty big move that might well do something to set the tone among high-end CEO’s. According to SEC filings, Cook reportedly has opted to take a pass on dividends he could have collected on over a million unvested shares. In total, that amounts to passing up about $75 million. Not that this is exactly going to leave Cook in the poorhouse — he’s paid a mind-boggling amount of money for the task of trying to fill Steve Jobs’s shoes. But still, it’s not trivial either. What should we make of it?

There are a couple of ways to think about this.

One has to do with shareholder confidence. Some have suggested that the decision is designed to show that Apple’s recent decision to pay a dividend wasn’t intended to benefit Cook himself. It is good for the investing public to know that the company is making decisions about things like dividends with the the best interest of shareholders in mind, rather than the best interests of the CEO. But then, Apple isn’t exactly suffering a crisis of shareholder confidence. If boosting the image of the company’s leadership is what you’re looking for, this might just be overkill.

But there’s another way to think of this, and that has to do with the good old-fashioned notion of honour. Call me a hopeless romantic, but I like to think that Cook’s decision might have something to do, as an unnamed source told the Telegraph, with setting an example for his fellow CEOs. Executive compensation has been in the spotlight almost continually for the last couple of years, and has even been the focal point of shareholder revolts. Maybe this is Cook’s way of saying, look, a high-end CEO doesn’t always have to squeeze every penny he can out of the company. And it’s entirely plausible, I think, that someone like Cook might make that decision — and send that signal — as a matter of principle.

“Honour” is the right moral category, here, because foregoing the cash is not something Cook is ethically obligated to do. He is fully within his rights, both legally and ethically, to take the dividend like other shareholders. But there’s arguably something good, something admirable, about attempting to shift the tone among high-end CEOs this way. It’s one thing to say that CEOs are overpaid. It’s quite another to set an example.

Will Cook’s move have any impact? Who knows. But it does seem like one more interesting attempt by the folks in Cupertino to get someone to “Think Different.”

Why $100-million Is Too Much

Filed under: accountability, boards, CEOs, compensation, corporations, energy, governance |

Comments (3) It was widely reported yesterday that former CEO of Nabors Industries Ltd., Gene Isenberg, will be the recipient of a $100 million severance payment. Except, he’s not leaving the company — he’s staying on as Chairman of the Board. Confusion and criticism has ensued.

For the most part, I think that executive compensation, even outlandish executive compensation, is in principle a private matter. If a bunch of shareholders want to pay their CEO a gazillion dollars — whether because they think he’s the one guy who can build long-term value or because they just think he’s a swell guy — well, that’s none of my business. I may think those shareholders are fools, or spendthrifts. But there’s little reason for me to be morally concerned. I don’t tell you how much to spend on your babysitter or your dry cleaning or your car. And I shouldn’t tell you how much to spend on your CEO.

In principle.

But two factors get in the way of applying my in-principle argument to the present case.

One factor begins with the observation that shareholders don’t, in fact, generally make the decisions regarding how much total compensation the CEO gets. That task is delegated to the Board of Directors, who in turn generally delegate it to their Compensation Committee. Now again, in principle, this is purely a private matter. If the Board isn’t serving the shareholders well, the shareholders have cause to complain, and (yet again, in principle) they can always fire the Board if they feel sufficiently poorly served. But we have ample evidence that shareholders very often aren’t well-served by boards. Add to that the fact that proper functioning of corporate governance (and hence of capital markets) is clearly a matter of public concern, and you have at least the beginnings of a public-interest argument for interference in what would otherwise be a private matter.

The other reason why excessive pay isn’t always a purely private matter has to do with the government’s (i.e., the public’s) role (and support of) an industry. Note, for example, that Nabors is an oil-drilling contractor. So the $100 million that Isenberg is getting isn’t merely a share of privately-gained profits. It’s a share of the profits from a heavily-subsidized industry.

So boards of directors do have some public obligations related to how they choose to compensate executives (even if, as I’ve argued before, outsized compensation isn’t automatically unfair). Corporate directors are not just part of private institutions; they’re part of a system justified, in part, by its public benefits. And the more they seek to gain private benefits in the form of subsidies, the greater their obligations to the public become.

Are CEO Salaries Too High?

It’s a perennial question, but one that still merits examination, given that one of the big complaints of the Occupy Wall Street movement has to do with the increasing wage disparity between the income-and-or-wealth of the top 1% vs the rest of us.

Economist Mike Moffat offered some new perspective on this yesterday, when he pointed out on twitter that “More NHLers earn 6 million+ a year than Canadian CEOs do.” And while sports commentators and fans sometimes roll their eyes at the astronomical salaries top athletes currently command, they’re not exactly taking to the streets in protest.

So why are people so outraged by executive compensation, but not by the salaries of sports figures?

There are two different questions to ask the question of “are CEOs paid too much.”

One is to ask whether CEO salaries are too high given what they contribute to the firms they manage. That’s a question that primarily concerns the shareholders and employees of a firm, who need to know whether their multi-million-dollar CEO is worth the money. Does hiring “Mr. A,” who insists on $6 million in pay, rather than hiring “Mr. B.”, who would work for a mere $3 million, bring more than an extra $3 million in offsetting revenue to the company? If so, then Mr. A is worth the money. If not, then he’s not. And my non-expert impression of the economic literature on this count is that evidence is mixed. Lots of CEOs aren’t worth the money. Lots are. The correlation, overall, is unclear.

The problem of how much to pay CEOs from this point of view, and what combination of kinds of payment to offer (cash, stock options, etc.), is hotly debated by top business scholars and economists. But it’s worth remembering that the money isn’t just all sitting there in a big pot, waiting to be distributed among the CEO, other workers, and shareholders. Each of those contribute some value to business. The hard question is how much.

The second way to look at CEO compensation is to ask whether CEO salaries are, in some sense, too high from a social point of view. That is, is it simply unconscionable that some people are paid that much? It is in this regard that Mike Moffat’s question about CEOs vs NHL players becomes interesting. Philosopher Robert Nozick famously raised this question of sports figures’ salaries over 30 years ago, as a way of investigating fundamental questions of justice. Modernizing Nozick’s example, we could look at a star player like the Pittsburgh Penguins’ Sidney Crosby, who was paid $9 million for the 2010-11 season. That’s a lot of money, in anyone’s eyes. But consider the process that results in that sum. Imagine how many fans Crosby has, and how many of them would each be willing to pay a dollar to see him play. It’s not hard to imagine 9 million fans, each happy — indeed, eager! — to hand over a dollar to see Crosby play. The net result is $9 million (taxable) in Crosby’s pocket, and no one else involved feels bad about it.

It’s not hard to translate Nozick’s example into business terms. Imagine a CEO who gets $9 million in total compensation. We’ll simplify and assume that’s all cash, which it never is. We’ll further simplify by looking only at the interests of employees (leaving out customers and shareholders). If the company is a fairly big one, and has 30,000 employees, then the Nozickean question is this: can we imagine each of those 30,000 employees voluntarily transferring $300 to their CEO for the value he adds to their lives? If that CEO leads the company to flourish — or, in tough economic times, even just to survive — then it’s at least plausible. And if so, then (says Nozick) there’s little grounds for complaint by employees, and even less grounds for complaint by anyone else. People might question the end result, but none can fault the fairness of the process that would have (or could have) resulted in it.

Now none of this amounts to saying that all is right in the world of CEO compensation. Many, many people inside the world of business will tell you that the situation is out of hand. And I agree. There have been outrageous abuses. The point here is just this: the fact that someone is highly paid isn’t automatically unfair. Sometimes it is unfair, and sometimes it isn’t. We need to look carefully, on a case-by-case basis, at what that individual contributes to the business they manage, and what that firm contributes to society.

See also: “Executive Compensation,” from the Concise Encyclopedia of Business Ethics.

The Complexity of Executive Compensation

Filed under: accountability, boards, CEOs, compensation, consultants, governance, pay, regulations |

Comments (2) Many jurisdictions have moved recently to give shareholders a “say on pay,” which typically means that companies are required to hold advisory (i.e., non-binding) shareholder votes on compensation. In other words, establishing executive pay remains the responsibility of the Board of Directors, but shareholders are given an opportunity to voice their approval or disapproval.

The Wall Street Journal recently reported that when given their say, shareholders at a resounding 98.5% of American companies have said “yes.” So it seems that, thus far, shareholders are hesitant to challenge Boards in their compensation decision-making.

This is not surprising, given the complexity of the decision that Boards face in setting executive pay. Setting executive pay is a task typically delegated to a Board’s “Compensation Committee.” Now consider the task faced by a Compensation Committee in establishing the total pay-and-incentive package offered to their CEO.

The question facing a Compensation Committee is this: what combination of cash, bonuses, equity, and perks should we put on the table in order to inspire our CEO to perform optimally? In practice, this is a pretty complex question, one not admitting of cookie-cutter solutions. A Comp Committee needs to consider, just for starters:

- pressures from shareholder (and other stakeholders),

- pressures from proxy advisory firms and various think-tanks,

- human psychology, including their particular CEO’s character and motivational levers,

- the managerial experience and expertise of Committee members,

- corporate objectives (profit, market share, sales, social responsibility, etc.),

- their company’s ‘risk appetite’ (roughly speaking, are they trying to incentivize their CEO to be bold, or conservative?),

- expert opinion about optimal compensation structures (which is deeply divided, to say the least).

The problem here is as much one of epistemology as it is one of ethics. Compensation Committees need to take an enormous amount of information and opinion and distill it into a decision that will work and that will be defensible in the face of enormous scrutiny.

Of course, there is no shortage of compensation consultants, ready and willing to help Compensation Committees with this task. But recent (not-yet-published) research at the Clarkson Centre suggests that many corporate directors are skeptical about the value of compensation consultants.

Given this complexity, it’s not surprising that shareholders — even sophisticated institutional shareholders — are so far pretty hesitant to do much second-guessing. Whether or not that’s a good thing is a separate issue.

Executives and their Income

Filed under: CEOs, compensation, contract, employees, finance, governance, pay |

Comments (11) I’ve blogged a number of times about what is commonly and loosely called “executive compensation.” The term is woefully imprecise. In point of fact, most “compensation” is not, in fact, compensation. The carrot dangled in front of a horse is not compensation; it is motivation. Compensation is what you give someone after the fact as reward for a job well done, or at least for a job that met contractual requirements. If I hire the neighbour’s kid to mow the lawn, and he does so, then I should compensate him. Most of the money garnered by senior executives at publicly-traded companies these days is not, in fact compensation. It’s money they get from selling shares in the company, shares granted to them as part of an effort to align their interests with the interests of shareholders.

The looseness of use of that word in the realm of finance is not at all unique. Witness the “bonuses” paid to AIG employees two years ago, which were not in fact performance bonuses at all but rather retention payments designed to keep key employees on what seemed at the time to be a sinking ship.

See more recently this piece by Peter Whoriskey for the Washington Post: With executive pay, rich pull away from rest of America. Here’s just a taste:

The top 0.1 percent of earners make about $1.7 million or more, including capital gains. Of those, 41 percent were executives, managers and supervisors at non-financial companies, according to the analysis, with nearly half of them deriving most of their income from their ownership in privately-held firms….

Notice that (contrary to the article’s title) the key factor in the growth of executive income here is not in fact “pay.” The key factor is investment income. And it’s not even “pay” in the loose sense of ‘money given by an employer,’ since there’s no indication here what portion of that investment income comes from shares in a CEO’s own company, say, versus a diversified portfolio. But it’s hard to hold Whoriskey to blame for the linguistic imprecision here; confusing pay and compensation and income is altogether standard.

The other point to be made here is about justice. According to Whoriskey, “…executive compensation at the nation’s largest firms has roughly quadrupled in real terms since the 1970s, even as pay for 90 percent of America has stalled…” Setting aside imprecision of language, that suggests a significant disparity — not disparity of outcomes (which are a given, here) but disparity of rate of improvement.

Now according to Leslie McCall, a sociologist quoted in Whoriskey’s story, people become concerned about such inequality “…when it seems that extreme incomes for some are restricting opportunities for everyone else.” And that may be true about people’s reactions. But of course, it’s very hard for people to tell when it is actually the case that extreme incomes for some are restricting opportunities for others. As economists often point out, income is not a fixed pile, waiting to be handed out. The way you distribute income actually changes the size of the ‘pie’ due to the way money incentivizes. Incentivizing executives with stock and stock options may on the whole be a failed experiment, but that doesn’t change the fact that it is impossible to know whether the average worker would be better or worse off had those incentives never been offered.